As long as you use an in-network facility, all costs associated with a screening colonoscopy should be paid by the health plan, including the bowel preparation drink, the facility fee, the doctor’s fee, and the anesthesiologist’s fee.

Insurance Companies

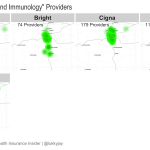

2018 Colorado Individual/Family Market Specialist Maps

Last week, I shared charts showing how many total providers are in each individual market insurer’s network, and compared that with total enrollment for each insurer. But the total number of providers doesn’t tell the whole story. Network adequacy issues still arise for specific consumers when an insurance plan might have many primary care providers, but… Read more about 2018 Colorado Individual/Family Market Specialist Maps

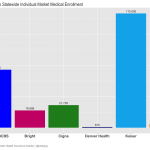

2018 Colorado Individual Market Enrollment and Total Medical Providers

2018 Connect for Health Colorado Individual Market Enrollment

2017 Rate Increases for Colorado Individual Health Insurance Market

EDIT, 9/25/2016: Rates were approved recently by the Colorado Division of Insurance. The following average rate changes (actual changes will vary by plan) will take effect January 1, 2017 for the seven carriers that will offer individual market coverage through the exchange. They will also apply off-exchange, as all of these carriers offer their plans both… Read more about 2017 Rate Increases for Colorado Individual Health Insurance Market

Commission cuts aren’t the same in states with state-run exchanges

EDIT, March 29, 2016: In addition to having state-run exchanges, there’s another factor involved here, which is much more likely to be the correct explanation. California, Colorado, Connecticut, and Kentucky are the four states that have taken regulatory action to prevent health insurance carriers from cutting commissions. Although my initial hypothesis wasn’t bad, direct action… Read more about Commission cuts aren’t the same in states with state-run exchanges

Understanding Drug Formularies On New Individual Health Insurance Plans In Colorado

Colorado residents only: Compare how each health insurance company covers your medication with our exclusive Colorado prescription drug formulary transparency tool. Opponents of the ACA have raised the issue of drug formularies as a negative aspect of the new ACA-compliant plans, complaining that the new plans won’t cover all of the medications people need. Just like many of their… Read more about Understanding Drug Formularies On New Individual Health Insurance Plans In Colorado

Carrier Contact Information And Updates For People Who Need To Pay January’s Premium

Today, January 10th, is the payment deadline for most Connect for Health Colorado policies with January 1 effective dates. A few carriers have pushed the deadline out a little bit: Updated Anthem Blue Cross and Blue Shield is moving the payment deadline to 1/31 for 1/1 effective dates. Delta Dental: January 15. Premier Access Dental… Read more about Carrier Contact Information And Updates For People Who Need To Pay January’s Premium

Updates For Colorado Residents Enrolling In Exchange Plans After December 23

Connect for Health Colorado is one of only five exchanges that extended the enrollment deadline for a January 1 effective date out beyond Christmas Eve. If you’re in Colorado, you have until the end of the day today (December 27) to enroll in a plan and get a January 1 start date. If you enroll… Read more about Updates For Colorado Residents Enrolling In Exchange Plans After December 23

Pediatric Dental on 2014 Individual Health Insurance Policies in Colorado

If you’re confused by the new pediatric dental requirements, you’re not alone. Here’s a rundown of how the ACA and HHS regulations impact pediatric dental coverage, with Colorado-specific details: The ACA defines pediatric dental coverage as one of the ten essential health benefits (EHBs) that must be covered on all new individual and small group… Read more about Pediatric Dental on 2014 Individual Health Insurance Policies in Colorado

Tobacco Use: ACA and Colorado Regulations

Back in January, I looked at the issue of tobacco use and the ACA from a mostly philosophical perspective. But we also wanted to provide a summary of what’s going on here in Colorado with regards to tobacco and the new health insurance policies that are available for 2014. Although the ACA has eliminated the practice of… Read more about Tobacco Use: ACA and Colorado Regulations

How Does Obama’s Policy Continuation Announcement Impact Colorado’s Individual Market?

By now you’ve probably heard about the Obama Administration’s compromise over the policy cancellation uproar. The fix that Obama has offered is that health insurance companies can extend existing plans for one more year, allowing them to continue to exist in 2014. This has been incorrectly reported in some media outlets as allowing carriers to continue… Read more about How Does Obama’s Policy Continuation Announcement Impact Colorado’s Individual Market?

Colorado Senator Udall Introduces Bill To Allow Individual Policies To Continue For Two More Years

Colorado Senator Mark Udall introduced legislation today that would allow people with individual health insurance to keep their existing policies for two more years – through the end of 2015 – regardless of any cancellation notices that have already been sent out. Udall’s Continuous Coverage Act is designed to smooth the transition to ACA-compliant plans…. Read more about Colorado Senator Udall Introduces Bill To Allow Individual Policies To Continue For Two More Years

Getting Past The Health Insurance Plan Cancellation Hysteria

Much has been said recently about how the ACA is causing a tidal wave of policy cancellations, and resulting in people losing coverage that they would prefer to keep. The frustrating part about this – as has generally been the case with every big uproar about the ACA – is that we’re not really getting… Read more about Getting Past The Health Insurance Plan Cancellation Hysteria

Fewer Plans Available In Exchanges In 2013, But Maybe That’s A Good Thing

At the end of September, just as the exchanges were about to open for business, HealthPocket created a comparison of the number of individual and family health insurance policies available in each state in 2013 and compared that with the number of policies that would be available in each state’s exchange in 2014. It’s an… Read more about Fewer Plans Available In Exchanges In 2013, But Maybe That’s A Good Thing

Government Shutdown: Is The Republican “Plan” Actuarially Feasible?

Although I’ve seen a lot of media references placing blame for the government shutdown squarely at the feet of House Republicans, I’ve also heard people saying that both sides are to blame and that the Democrats could have “compromised.” I’ve just finished reading the text of the House amendment to H.J. Res. 59. This is the amendment that would have “delayed Obamacare” by a year.

There are a couple specific aspects of the ACA that House Republicans were trying to delay or delete. The most significant is the individual mandate (keep in mind that this has been challenged all the way to the Supreme Court and found to be Constitutional), which the amendment would postpone until 2015. [The amendment also contains some other provisions regarding health insurance for Congress and the President, which I’ll address tomorrow.]

The initial provisions of the ACA started to take effect in 2010. January 1, 2014 is about 3.5 years after that, so the individual mandate had a significant built-in delay. But let’s assume for a moment that the Democrats wanted to accept this “compromise” and allow the individual mandate to be delayed until 2015. What would that have involved from a practical standpoint?

An actuarial nightmare

Back in the spring of this year, health insurance carriers all across the country were scrambling to submit rates and plan designs for review. There were some delays, and some carriers ended up having to redo their rates and submit them again, but by the middle of August we had a pretty good idea of what plans were going to be available in the Colorado marketplace (exchange) – and news was also coming in from lots of other states. This was six weeks before the marketplaces opened, and a full 4.5 months before the new policies were going to be effective. Once the rates were finalized, they had to be loaded into each marketplace’s online quoting software so that they would be available to navigators, brokers and applicants once the marketplace opened for business.

This whole process took many months. Creating the ACA-compliant plan designs and doing the actuarial work to price them was not something that happened overnight. Carriers were working on this early in the year, getting their plan design and rate info ready to submit in the spring. And then the rate reviews, final approval, and user interface updates added to the time frame.

So let’s go back and look at the Republican “compromise” of delaying the individual mandate for a year. All of the new plans and rates that actuaries, marketplaces and Divisions of Insurance have been working with this year are designed around the basic concepts of the ACA: Policies  must be guaranteed issue (a huge change from the way policies have historically been issued in the individual market, where underwriting has been part of the process in all but five states), they can only be issued during open enrollment or following a qualifying event (loss of other coverage, birth, adoption, marriage, divorce), and the individual mandate is expected to generally increase enrollment.

must be guaranteed issue (a huge change from the way policies have historically been issued in the individual market, where underwriting has been part of the process in all but five states), they can only be issued during open enrollment or following a qualifying event (loss of other coverage, birth, adoption, marriage, divorce), and the individual mandate is expected to generally increase enrollment.

Removing any of these elements would drastically change the pricing of the policies and basically mean that the actuaries would have to start over. Incidentally, the House Amendment does not mention delaying the requirement that individual health insurance be guaranteed issue starting in 2014. To roll out guaranteed issue coverage without the individual mandate would mean that rates would be significantly higher for the people who do opt to purchase a plan. But regardless, removing one of the primary elements upon which the 2014 rates have been based would mean a complete do-over of the actuarial process of pricing the new policies.

But what about just keeping things the way they are? Can’t we just keep our 2013 plans and roll them into 2014 with no changes?

No. Remember, the House Amendment to “delay Obamacare” (that’s the language most often used in the media and by lawmakers themselves) would actually just delay the individual mandate. It doesn’t delay the other crucial aspects of the ACA that guided plan design for 2014. So policies would still have to provide essential health benefits. They would have to be guaranteed issue and priced the same regardless of gender (in Colorado, this has been the rule for almost three years now, but the ACA bans it everywhere).

So current 2013 policies could not continue to be issued in 2014. They’re not compliant in terms of plan design, even if actuaries were able to perform a miracle and redo all of the pricing in the next few weeks.

That puts us back to starting over with the new ACA-compliant plans that carriers created months ago, and trying to reprice them for 2014 to reflect a delay in the individual mandate. Remember that the actuaries have to come up with the pricing (not a quick process), DOIs and marketplaces have to review the pricing, and then the final rates have to be uploaded to quoting systems (both marketplace systems and private “off-exchange” quoting systems) and added to printed sales materials in time for consumers to be able to use them. For 2014 plans, this process started early in 2013. Starting over at the beginning of October would have been mission impossible.

Consumers have generally always been able to submit applications one to two months prior to the effective date they want. A lot of people wait until the last minute, but quotes are available several weeks out. That means that if actuaries were to start over at the beginning of October and redo everything, the entire process would have to be completed by mid November at the latest in order for accurate pricing information to be available for consumers looking for a January 1 effective date. The House Amendment did not mention delaying the opening of the marketplaces, so it’s unclear what lawmakers wanted the marketplaces to do. Would plan information still be available in early October, but with no rate data?

To say that this was a poorly planned amendment is an understatement. It was political posturing designed to appeal only to people who “hate Obamacare” (and unfortunately, some of those people are woefully uninformed about the law). It had no basis in actuarial reality, and would have thrown […]

Renewal Options for Each Individual Health Insurance Carrier in Colorado

Last week I explained how early renewal at the end of 2013 might be a good option for some people who have individual health insurance. If you’re happy with your coverage and aren’t going to qualify for a subsidy in the Colorado exchange, keeping your existing plan for most of 2014 might be a good way to save some money on premiums. This is especially true for people who prefer very high deductibles, as those plans are generally not ACA compliant and thus will not be available for purchase after the end of 2013. But if your carrier allows it, you can keep your current policy until it renews in 2014, and switch to an ACA compliant plan at that time. For people with plans that renew late in the year, this could mean keeping a lower-cost, higher deductible policy for most of 2014. If you’ll be eligible for a premium subsidy, it’s definitely worth your time to compare a subsidized exchange plan with what you have now. But if you’re happy with your coverage and you’re going to be paying full price for an ACA compliant plan, check with your carrier to see about keeping your current plan in 2014.

Keep in mind that each Colorado health insurance carrier is doing things a little differently in terms of 2013 renewals heading into 2014. It’s important to check with your carrier to make sure you’re aware of what steps you need to take – don’t assume that your plan will automatically renew – or automatically not renew. The Colorado Division of Insurance has left a lot of leeway for carriers to determine their own protocol for renewals going into 2014. There is no state requirement that existing policies be cancelled as of the end of 2013, although some carriers have opted for that as a default. All plans must be ACA-compliant by January 1, 2015. So when your policy renews in 2014, you will have to transition to an ACA compliant plan. But the date of that renewal can be anytime from January to December.

Here’s a brief summary of what we have heard so far from some of the main carriers in Colorado. This is subject to change, so check with us or your carrier before you make a decision.

Anthem Blue Cross Blue Shield: The default is for your plan to just keep its current renewal date and continue unchanged until that date in 2014. But Anthem is also offering insureds an option […]

Early Renewal Provides A Good Alternative For 2014

Over the last few years, opponents of health care reform have often exaggerated – and sometime outright lied about – the potential negative aspects of the reform law. This has resulted in a public that is often woefully misinformed about what the law does and does not do. But the spin is not limited to just opponents of the law. Sometimes ACA supporters spin things too. This Huffington Post article from a few months ago is a good example. The title, “Aetna seeks to avoid Obamacare rules next year” is designed to play on the general unpopularity (and over-estimation of perceived profits) of insurance companies. When you read a little further, you find that Aetna is reaching out to brokers and insureds to let them know that Aetna will be allowing members to opt for an early renewal in December of this year – if they want to keep their current policy until December 2014.

Why is this being portrayed as a bad thing?

It is indisputable that people who are healthy, buy their own health insurance, won’t qualify for subsidies and prefer high deductible health plans are going to have higher premiums for ACA-compliant plans than they have now. Some of these people don’t mind high deductibles. They don’t consider their policy to be skimpy or junk insurance just because it isn’t ACA compliant. You might have seen headlines about how only a tiny fraction of existing individual health plans meet the requirements that the ACA will impose next year, but that doesn’t mean that the existing plans are junk. If you look closely, you’ll see that when it comes to basic medical benefits, a lot of individual plans offer coverage that is in line with ACA regulations. But benefits like dental and vision coverage for children (required on ACA-compliant plans starting next year) are usually not part of individual coverage (Many plans allow applicants to select add-on dental and vision coverage, but a lot of people find that it’s more cost effective to pay for dental and vision out of pocket rather than paying for dental/vision insurance. Remember, nothing is free. And the more likely you are to use an aspect of your coverage, the higher your premiums will be in order to cover the cost. So coverage for something like dental and vision checkups – which people plan to use – has to be priced accordingly). In many states, maternity coverage is one of the most significant medical benefits missing from a lot of individual plans. But in Colorado we’ve had maternity on all plans for more than two years now.

There are absolutely some bad health insurance plans on the market, with skimpy coverage, limited networks and lots of fine print. But there are also lots of good quality health insurance plans and reputable carriers. And there are plenty of people who are not going to qualify for subsidies next year (roughly half of the people who currently buy individual health insurance). If those people currently have – and are happy with – a high deductible plan that is less expensive than what they would have to pay for an ACA-compliant plan, there’s no reason that they shouldn’t be able to keep their plan as long as possible in 2014. The law requires coverage to be ACA-compliant when a policy renews in 2014. Carriers that are offering early renewals in December are providing good customer service, especially for insureds who […]

Your Health Insurance Will Probably Change in 2014

I frequently come across FAQs on various websites with a question along the lines of: “Do I have to switch to a new health insurance plan if I like my existing one?” And almost always, the answer is something like this: “No. The ACA allows grandfathered health insurance plans to continue unchanged, so if your plan was in effect when the ACA was signed into law on March 23, 2010 and has not been significantly changed since then, it will be considered “qualified coverage” and you can keep it”.

This is frustrating to read, because I’m sure that people who aren’t familiar with the details of health care reform might just see that first word – no – and not pay attention to the significant caveat that follows it. Adding to the confusion is the partially true statement President Obama made in 2009, saying “If you like your health care plan, you will be able to keep your health care plan. Period. No one will take it away. No matter what.”

The problem is that people who currently have health insurance might think that they can keep their plan – even if they’re not on a grandfathered plan – because there’s a lot of confusion about what exactly a grandfathered plan is. In 2012, just under half of people who get their health insurance from an employer were on a grandfathered plan, but that number is dropping and will continue to do so as plans change. There’s no way to know whether your health plan is grandfathered without calling your carrier and asking. A plan that was grandfathered as of 2011 might not be so today, since changes to the plan can happen at any time and can cause a plan to lose its grandfathered status.

The really bad health insurance plan that I wrote about earlier this year might be a grandfathered plan that was in effect when the ACA was signed into law. Insureds may have joined after that date and still be on a grandfathered plan. (although that still doesn’t explain the $5 million lifetime max that was being marketed on that plan as of this year – even grandfathered plans are not allowed to have lifetime maximums).

But especially in the individual market, health plans are constantly being redesigned. The way the process works in Colorado – and in many other states – is that existing plans are retired, or “sunset” and new ones are introduced. In most cases, insureds are allowed to remain on the sunset plan. If the carrier does away with the plan completely, they have to offer the plan’s insureds the option to purchase any of the other plans the company offers, guaranteed issue. So most carriers have traditionally let insureds remain on sunset plans, but the plan becomes a closed block, which means that no new insureds are being added to the pool. The result is usually that over time, premiums within a closed block start to rise faster than premiums in other plans that are enrolling new members (keep in mind that in the individual market, medical underwriting has long been used to make sure that new members are relatively healthy. So for individual plans, members who have been on the plan the longest tend to have higher claims expenses than new members). This leads healthy insureds who are on sunset plans to seek coverage in another plan in order to lower their rates.

There are lots of reasons for new plan designs: It’s a way for carriers to create product differentiation (especially true in robust markets like we have in Colorado). New plan designs also allow carriers to create products with lower premiums, as they’re well aware that price is one of the most important factors when consumers are shopping for coverage (a good example is the trend over the past decade towards health plans with separate prescription deductibles instead of integrated Rx deductibles or Rx coverage with traditional copays). New plan designs also […]

Why ACA Compliant Plan Premiums Will Vary Significantly In 2014

David Williams did an excellent job with the most recent edition of the Health Wonk Review – be sure to check it out. One post that everyone should read comes from Health Affairs Blog, and was written by Joel Ario, Adam Block and Ian Spatz. They dig into the details of Silver plan premiums in four major US cities, finding lots of variation in pricing in some areas, and surprisingly little variation in others. As premiums have been slowly publicized over the last several weeks, I’ve seen numerous articles describing rates for ACA-compliant plans and how they vary from one plan to another within the same metal designation. But the Health Affairs article is the most thorough and helpful that I’ve read. The authors not only explain the details, but they also provide five very well-reasoned explanations for rate variation. If you’re confused about premiums for ACA-compliant plans, this article is a must-read. It’s also helpful in terms of helping people understand how plans can differ – even at the same metal level – beyond the basic deductible/copay amounts.

Wide variation in health insurance rates is nothing new. When I run current quotes (not yet 2014 ACA-compliant) for my own family, I get 11 pages of results, with prices ranging from $238/month to $1889/month. Much of that is explained by the vast differences in deductibles ($10,000 for the lowest priced plan, $500 for the highest), but even if I focus on plans that all have the same deductible ($5000, just to pick a middle-of-the-road number), I still get rates that range from $325/month to $924/month. Plan designs can vary greatly from one carrier to another, and provider networks make a big difference in terms of explaining premium variation from one area to another within a state (as an example here in Colorado, the carriers that offer the best rates in the Denver metro area and along the front range are typically not the same carriers that offer the best rates in the mountains or even in nearby Boulder, and much of the variation has to do with provider networks).

So it’s not at all surprising that rates will be significantly different from one carrier to another next year, both in and out of the exchanges. In most states […]

Colorado Health Insurance Options On the Exchange in 2014

Although we’re still at least a week away from knowing the specific details on rates and plan designs for policies that will be sold in the Connect for Health Colorado exchange, the Division of Insurance has approved 242 plans that will be available in the exchange from 13 Colorado health insurance carriers. In late May, the number of carriers stood at 11 and the number of plans was 250+. But as we noted last week, there was still a lot going on behind the scenes over the summer, and some carriers had to resubmit plan information that was not accepted in the spring. The final count is 150 plans that will be available to individuals and 92 for small groups (keep in mind that this is just for plans within the exchange. There will be lots of other ACA-compliant plans available outside the exchange).

The plans for individuals will be available from ten different carriers (All Savers, Cigna, Colorado Choice, Colorado Health Insurance Cooperative, Denver Health Medical Plan, HMO Colorado (Anthem), Humana, Kaiser, New Health Ventures and Rocky Mountain HMO). Although there are some new names in this list, there are also plenty of familiar ones (All Savers is a UnitedHealth company, which means that the main carriers that currently sell policies in the individual market in Colorado will all be represented in the exchange). Although we haven’t yet seen the final premium and plan details, it appears that Colorado will continue to have a robust individual health insurance market in 2014, both in and out of the exchange.

For consumers who will qualify for a subsidy, the exchange is definitely the place to be – subsidies are only available in the exchange. Consumers who do not qualify for a subsidy (either because their income is too high or because they have access to an employer group plan that is technically “affordable” but might actually be outside of their budget) can shop within the exchange (via an approved broker or directly through the exchange) or they can […]

Assurant and UnitedHealth Still Available In Colorado Individual Market

The Colorado Division of Insurance has announced that finalized health insurance rates won’t be available until the middle of August – about two weeks after the originally-scheduled August 1 release date. The preliminary rates, carriers and plan designs were announced in June, and it’s likely that the final rates will be in the same basic range. When we first saw the list of carriers that were going to be providing individual health insurance in Colorado starting in October (for 2014 effective dates), we were surprised to see that UnitedHealth Care was only listed as a carrier for small group plans (they have had a strong presence in the individual health insurance market in Colorado for many years, both as Golden Rule and UnitedHealthOne). And we also noticed that Assurant (Time) was not included at all in the list of carriers that had submitted rates and plans to the DOI earlier this year.

We’ve recently found out that Assurant will indeed continue to offer individual health insurance in 2014, outside of the exchange. They submitted rates and plans in May but the submission was incomplete and had to be refiled, which is why they were missing from the data that was released in June. The Assurant details should be included with the finalized rate information that will be released in mid-August.

In addition, UnitedHealth Care will be offering individual health insurance in the Connect for Health Colorado exchange, under the name All Savers Insurance Company. This was included with the June data, but many people might have been unaware that All Savers Insurance is a UnitedHealth Care company.

We wanted to clarify this information in case you’re looking for an individual policy from either of these companies. More info will be forthcoming once we have the finalized rate data, so stay tuned.

A Midsummer Wonk’s Dream

Welcome to the Midsummer Health Wonk Review! It’s always a pleasure to host, and this edition actually isn’t a Shakespeare theme, but it is jam-packed with excellent articles from some of the best writers in the healthcare blog world. The HWR had a break before this edition and will have a hiatus after this one too. We’re starting things off with a few articles that help to shed light on some aspects of health care reform that should be straight-forward but sometimes get a bit convoluted with political rhetoric. Then we’ve got several posts about corruption in healthcare and healthcare policy, and lots of posts that provide contrasting and well-reasoned viewpoints on healthcare reform and healthcare in general. We’ll keep things cool with some winter and spring pictures we took around us here in Northern Colorado. Enjoy!

In an excellent piece debunking popular “wisdom” regarding immigrants and healthcare, Joe Paduda of Managed Care Matters explains that when it comes to the Medicare Trust Fund, immigrants put in a lot more than they take out: In 2009, immigrants paid in 14.7% of trust fund contributions but only accounted for 7.9% of its spending, with a net surplus of almost $14 billion. US-born people accounted for a deficit of almost $31 billion in the Medicare Trust Fund that same year. This appears to be a long-term trend: From 2002 to 2009, immigrants contributed $115.2 billion more to the Medicare Trust Fund than they received in Medicare benefits. Joe goes on to explain the details and warn those who rally behind strict immigration reform that they may want to rethink their position. Our Medicare Trust Fund would be in a lot worse shape without the immigrant population.

In an excellent piece debunking popular “wisdom” regarding immigrants and healthcare, Joe Paduda of Managed Care Matters explains that when it comes to the Medicare Trust Fund, immigrants put in a lot more than they take out: In 2009, immigrants paid in 14.7% of trust fund contributions but only accounted for 7.9% of its spending, with a net surplus of almost $14 billion. US-born people accounted for a deficit of almost $31 billion in the Medicare Trust Fund that same year. This appears to be a long-term trend: From 2002 to 2009, immigrants contributed $115.2 billion more to the Medicare Trust Fund than they received in Medicare benefits. Joe goes on to explain the details and warn those who rally behind strict immigration reform that they may want to rethink their position. Our Medicare Trust Fund would be in a lot worse shape without the immigrant population.

And if you’re curious about the implementation track for the ACA (and understandably confused by the constant talk of repeal, delay, replace, etc. that we keep hearing from some politicians) Linda Bergthold has what I consider to be a straight-forward and factual review of the situation. To sum it up, she’s predicting that the employer mandate will go into effect in 2015, as currently scheduled (following a one-year delay, but not a repeal), and that the individual mandate will be implemented in 2014, as planned. And while some states that delayed the creation of an exchange marketplace will likely have a tougher time getting everything up and running by 2014, the exchanges will be operational next year. I imagine there will be some bumps in the road as the ACA is fully implemented over the next few years. But we can work on ironing those out as we go – there’s no need to start from scratch.

Although the exchanges are likely to be successful in the long run, it won’t be without significant effort on the part of the people running them. At Health Affairs Blog, Barbara Markham Smith and Jack Meyer explain their recommendations for strategies that can help the exchanges be successful both out of the gates and for the long haul. They discuss pricing (don’t make it too high!) as well as communication/advertising programs that need to be unified, clear, concise and nation-wide in order to generate awareness and interest in as many people as possible.  (Unfortunately, there’s a significant portion of the country’s leadership who seem to want the exchanges to fail – even to the detriment of the American people – and are content to spread mis-information about the entire law. This is a considerable hurdle that the exchanges will have to overcome.) Barbara and Jack recommend a temporary respite from the tax reconciliation that will be done to determine whether a person or family that received a subsidy is required to pay back a portion of it due to increased income compared with the prior year. And they also call for fostering increased competition and CO-OP creation in the states have not yet done so. All in all, pretty solid ideas for success in the exchanges and policy-makers would be wise to take heed.

(Unfortunately, there’s a significant portion of the country’s leadership who seem to want the exchanges to fail – even to the detriment of the American people – and are content to spread mis-information about the entire law. This is a considerable hurdle that the exchanges will have to overcome.) Barbara and Jack recommend a temporary respite from the tax reconciliation that will be done to determine whether a person or family that received a subsidy is required to pay back a portion of it due to increased income compared with the prior year. And they also call for fostering increased competition and CO-OP creation in the states have not yet done so. All in all, pretty solid ideas for success in the exchanges and policy-makers would be wise to take heed.

I think of Dr. Roy Poses as the healthcare blog world whistleblower – he can always be counted on to expose nefarious acts in the healthcare industry, and Health Care Renewal is a must-read blog. Here is his take on the recent Transparency International poll that found 43% of US respondents believe that the US healthcare system is corrupt, and that 64% believe that the government is run by big money and special interests. Roy notes that unfortunately, most of the media coverage of the Transparency International poll has focused on world-wide data and/or specifics from far-away lands. Instead of focusing on our own serious problems with corruption in healthcare, it seems that a lot of media outlets (keep in mind that media is sometimes beholden to special interests too…) prefer to present the problem as something that happens in other countries as opposed to something that we need to work on here in the US.

Continuing with the corruption theme, Eric Turkewitz of the NY Personal Injury Law Blog shares a multi-part series about Dr. Katz, who has been rebuked for lying on the stand in a personal injury trial that resulted in a mistrial because of the doctor’s actions. Central to the issue is the practice of independent medical exams (with the word “independent” being very loosely used in this case) conducted by doctors who are hired by insurance companies when they are defending personal injury cases. In the case that Eric is writing about, the doctor makes a 7 figure income  from his medical-legal practice, but in one case that has been made public, he grossly over-stated the amount of time he spent with a patient (he claimed it was 10 – 20 minutes, but a secretly-made video recording of the visit showed that it was under two minutes). Eric has looked at additional data and found that the average length of Dr. Katz’s exams was around 4 minutes. Additional details on this story are here. Wow. The doctor was obviously concerned first and foremost with money, but the insurance companies who hired him were likely not doing due diligence to make sure that he was providing accurate data. They may have been more concerned with finding a doctor who would tell them what they wanted to hear rather than the actual details of the patients’ medical cases. Sad all around, but sadder still is the fact that it’s probably not all that unusual.

from his medical-legal practice, but in one case that has been made public, he grossly over-stated the amount of time he spent with a patient (he claimed it was 10 – 20 minutes, but a secretly-made video recording of the visit showed that it was under two minutes). Eric has looked at additional data and found that the average length of Dr. Katz’s exams was around 4 minutes. Additional details on this story are here. Wow. The doctor was obviously concerned first and foremost with money, but the insurance companies who hired him were likely not doing due diligence to make sure that he was providing accurate data. They may have been more concerned with finding a doctor who would tell them what they wanted to hear rather than the actual details of the patients’ medical cases. Sad all around, but sadder still is the fact that it’s probably not all that unusual.

And for a little more on the cronyism/corruption topic (maybe those corruption figures Roy mentioned from the Transparency International poll were skewed a bit too low?), Hank Stern of InsureBlog writes about agencies and individuals who have been involved with the Obama Administration for some time, and are now finding themselves in lucrative financial and/or influential positions as the ACA gets implemented. In other words, business as usual in the government. Government appointments, grants, etc. are often awarded this way (ie, appearing to be rewards for donations and/or loyalty), in every administration, regardless of which party is in power. There’s ample room for opponents to cry foul, but it also has to be pointed out that presidents and secretaries and others in power have to be able to select people they trust for top leadership positions. And trust is earned over time. There’s a fine line between selecting the right candidate for the job, having that person be someone trusted by the top officials, and avoiding cronyism. I don’t know what the right answer is, but it’s easy to see how the appointments and grants and leadership roles being handed out with the ACA could be construed as rewards for political support and loyalty.

At Health Beat, Maggie Mahar writes a thoughtful and thorough review of Miriam Zoll’s Cracked Open: Liberty, Fertility and the Pursuit of High Tech Babies. After reading Maggie’s article, I’m eager to read the book itself (Maggie leaves a bit of a cliff hanger at the end…). Assisted reproductive technology is certainly a blessing to many families. But it can also be fraught with problems that stem from both overly-optimistic expectations on the part of patients (and society in general), over-promising on the part of providers, and a medical field that is largely unregulated and often not covered by health insurance policies.

At Health Business Blog, David Williams explains his skepticism about DealWell, a new Priceline-style website for healthcare services. I am very much in favor of increasing transparency in healthcare pricing and moving away from the proprietary pricing system we have now, where even the most dedicated patient “shoppers” can find it impossible to obtain real healthcare prices before having a procedure. And to that end, I love the idea of a website where people can bid on the care they need and providers can accept or decline the offer depending on their current workload and the payment offered. But David makes some excellent points about the downsides: not being integrated with health insurance is a big one, especially since nearly everyone will have to have health insurance starting in 2014 (even if a procedure is lower than your deductible, it makes sense to stay in network and have the amount you pay be credited towards your deductible, in case you need additional care later in the year). Although DealWell might be a good option for people looking for one-time services that aren’t covered by health insurance (such a LASIK or a dental implant, for example), it’s probably not going to be the next big thing in healthcare price transparency.

idea of a website where people can bid on the care they need and providers can accept or decline the offer depending on their current workload and the payment offered. But David makes some excellent points about the downsides: not being integrated with health insurance is a big one, especially since nearly everyone will have to have health insurance starting in 2014 (even if a procedure is lower than your deductible, it makes sense to stay in network and have the amount you pay be credited towards your deductible, in case you need additional care later in the year). Although DealWell might be a good option for people looking for one-time services that aren’t covered by health insurance (such a LASIK or a dental implant, for example), it’s probably not going to be the next big thing in healthcare price transparency.

Over at Disease Management Care Blog, Jaan Sidorov takes a closer look at the glowing picture painted by CMS regarding ACO pilot programs, digs a little deeper, and gives us a slightly less rosy view of the results. And there’s even a T-Rex analogy, to keep things even more interesting. Jaan points out that the ACOs that didn’t meet the pilot program goals are likely feeling the sting of losing millions of dollars, since the initial investment costs are not cheap. Although 9 of the 32 pilot ACO providers have said that they want to leave the program, I wonder if results will be better as time goes by, mitigating the initial investment costs somewhat? Stay tuned.

Julie Ferguson of Workers’ Comp Insider writes about the July 6th 777 crash at SFO, detailing how the flight attendants did an excellent job of putting their emergency training into practice, saving lives in the process. Julie notes that while it’s easy to shrug off emergency plans simply because we rarely come face-to-face with an emergency, such preparedness can mean the difference between life and death. Does your business have a solid plan in place to deal with emergencies? Has everyone at the business been trained on it? How fast can your building be evacuated if necessary? All good things to think about.

Writing at Health Access Blog, Anthony Wright discusses the one-year delay of the employer mandate portion of the ACA that will require employers with more than 50 employees to provide health insurance to eligible full-time workers. Anthony makes some very important points: the delay doesn’t impact anyone’s eligibility for health insurance and/or subsidies. People who would have been offered health insurance from an  employer with the employer mandate in place will still be able to get coverage through their state’s exchange – and if they make up to 400% of the federal poverty level, they’ll qualify for subsidies to help pay for it. In addition, the vast majority of large employers in the US already offer health insurance to their employees and have historically done so without a mandate requiring it. It’s unlikely that a large amount of those employers will suddenly drop their coverage in 2014. But Anthony goes on to note that if the delay were extended for additional years, it could begin to destabilize the financial foundation of the ACA and employers might begin to shift more workers onto exchange plans, relying on tax-funded subsidies to foot a portion of the bill.

employer with the employer mandate in place will still be able to get coverage through their state’s exchange – and if they make up to 400% of the federal poverty level, they’ll qualify for subsidies to help pay for it. In addition, the vast majority of large employers in the US already offer health insurance to their employees and have historically done so without a mandate requiring it. It’s unlikely that a large amount of those employers will suddenly drop their coverage in 2014. But Anthony goes on to note that if the delay were extended for additional years, it could begin to destabilize the financial foundation of the ACA and employers might begin to shift more workers onto exchange plans, relying on tax-funded subsidies to foot a portion of the bill.

The Healthcare Economist, aka Jason Shafrin, brings us a great summary of health insurance in China over the past half century. Until the end of the 1970s, there were three main health insurance systems in China that covered nearly everyone. But the wheels started to come off after that; by 1998 almost half of the urban population had no health insurance, and by 2003, 95% of the rural population in China was uninsured. In the last ten years, China has tackled health care reform in order to try to remedy the problem. While plenty of progress has been made, there is still a long way to go.

Jared Rhoads has written a review of The Autistic Brain by Temple Grandin. His review is a good read, and the book looks like it is as well. Professor Grandin teaches at Colorado State University – my alma mater – and consults for the livestock industry as well as being a bestselling author. She’s an inspiring and accomplished person even without taking into account her own autism. Her book combines her personal  experiences with the latest that science has to offer us with regards to autism. If you’re interested in autism, Jared’s summary is that this book is a good place to start learning more. I’m adding it to my list of books to read, so thanks for the tip Jared!

experiences with the latest that science has to offer us with regards to autism. If you’re interested in autism, Jared’s summary is that this book is a good place to start learning more. I’m adding it to my list of books to read, so thanks for the tip Jared!

John Goodman lays out some of the results of the ACA thus far (fair enough, but keep in mind that most of the law hasn’t been implemented yet). He details some positives and negatives, both expected and unintended, although his overall take is that the ACA is not a great solution. Strongly worded opinions about the ACA will likely meet with a round of applause from one side of the political spectrum, and boos from the other side. But regardless of your position, I would say that it’s tough to argue with John’s point about high deductible, consumer-driven health plans. I think he’s correct in saying that they’re probably going to be quite popular starting in 2014, when they will be among the least-expensive plans available. This is probably particularly true among people who won’t qualify for subsidies.

That’s it for this mid-summer edition of the Health Wonk Review. Many thanks to Julie and Joe for keeping such a great blog carnival going all these years! The HWR now has a summer hiatus. Don’t miss the next edition on August 15th, which will be hosted by David Williams at Health Business Blog.

Clearing Up Confusion Around The Health Insurance Provider Fee

One of the funding mechanisms for the health insurance exchanges is the implementation of the health insurer fee that will go into effect in 2014. I’ve seen this referred to as a health insurance provider fee (a bit confusing as it might lead people to believe that the fee is imposed on medical providers rather than insurers), a health insurance industry fee, and an ACA health insurance carrier fee, among others. But whatever you want to  call it, the fee is an amount that will be collected from health insurance carriers starting next year, and the funds will be used to help pay for the state and federal health insurance exchanges.

call it, the fee is an amount that will be collected from health insurance carriers starting next year, and the funds will be used to help pay for the state and federal health insurance exchanges.

The fee will generate $8 billion in 2014, and will increase each year up to $14.3 billion in 2018. After that, it will increase annually in line with health insurance premiums. Insurance carriers will be responsible for remitting their share of the fee, which is calculated based on the insurer’s total collected premiums from the prior year.

As is generally the case with any new fees or mandates that increase costs for insurance companies, this fee will be passed on to companies and individuals who purchase policies. However, it won’t necessarily be easy to determine how much the fee is impacting your health insurance premiums, since many carriers are expected to just roll the fee into their total premiums.

In Colorado, Rocky Mountain Health Plans has stated that they will be adding the health insurance provider fee as a separate line item on their bills in an effort to be as transparent as possible. They will begin collecting the fee next month (July 2013) in order to spread the fee over a longer time horizon and thus lessen the impact on next year’s premiums. Carriers can choose to wait to begin collecting the fee, but the total amount collected will be the same regardless: Roughly 2% – 2.5% of total premiums in 2014, and 3% – 4% of total premiums in future years. In the individual market, RMHP will be collecting $4.12 per member per month, for the rest of 2013. If you have a SOLO plan with RMHP and notice a line item on your bill labeled “Health Insurance Providers Fee”, now you’ll know what it is (be aware that the total collected is per member per month, so if you have a family of five on a RMHP policy, your bill will reflect a charge of $20.60/month starting in July). If you have coverage with another carrier, you’ll still be paying the fee (some carriers […]

Networks And Carriers Are Part Of The Big Picture With Exchanges

[…] Aetna, United and Cigna are all absent from the CA exchange, and Dan looks into several reasons why some of the bigger carriers might have opted not to sell in the exchange on day one, and why some large provider networks are not going to be covered by plans sold in that state’s exchange.

Here in Colorado, Aetna stopped selling individual policies a couple years ago, so we weren’t expecting them to be in the state’s exchange, Connect for Health Colorado. United Healthcare has been a mainstay in the Colorado individual market, and while they submitted numerous plans to the DOI for small group products, they are all to be sold outside of the exchange and there don’t appear to be any individual plans in their new lineup. Cigna, however, will be selling individual plans both inside and outside of the exchange in Colorado.

Here in Colorado, Aetna stopped selling individual policies a couple years ago, so we weren’t expecting them to be in the state’s exchange, Connect for Health Colorado. United Healthcare has been a mainstay in the Colorado individual market, and while they submitted numerous plans to the DOI for small group products, they are all to be sold outside of the exchange and there don’t appear to be any individual plans in their new lineup. Cigna, however, will be selling individual plans both inside and outside of the exchange in Colorado.

We’ve heard from carrier representatives – who are familiar with multiple state exchanges – that Connect for Health Colorado has been particularly great to work with, and that is no doubt part of the reason Colorado will have a large number of carriers and policy options available within the exchange. We’re happy to be in a state that has been actively working on healthcare reform for several years, and that moved quickly to begin building an exchange and implementing the ACA as soon as it was passed.