A quick overview of how individual health insurance will change in 2014 due to the Affordable Care Act (ACA).

Archives for February 2013

Health Insurance Premiums Coming To A W2 Near You

I’ve noted many times on this blog that one of the difficulties faced by proponents of health care reform is the fact that a lot of Americans are somewhat shielded from the actual cost of health insurance because a portion of their health insurance is paid for by their employer. And when we talk about… Read more about Health Insurance Premiums Coming To A W2 Near You

Pre-Existing Condition Insurance Plans (PCIP) Stop Accepting Applications

[…] Fortunately, Colorado has CoverColorado, which will continue to operate. But if you live in a state that has a federally-funded but state-run high risk pool and you need to secure coverage through it, make sure that you get your application submitted before March 2, 2013.

Looking beyond the PCIP, I have to wonder how this bodes for the health insurance exchanges/marketplaces and the entire individual health insurance market once plans are all guaranteed issue. The cost of caring for people with pre-existing conditions is high – there’s not really a way around that unless we can start making inroads into reducing the actual cost of care. And although guaranteed issue health insurance is definitely a step in the right direction in terms of getting access to healthcare for everyone, it’s also going to result in higher health insurance claims, and almost certainly higher health insurance premiums in the individual market. Hopefully the individual mandate will be successful at bringing enough young, healthy people into the insurance pool to offset the higher cost of care for people with expensive pre-existing conditions. With enough healthy people enrolled, the guaranteed issue individual market could be a solid health insurance pool. But if the balance shifts more towards unhealthy people, the individual market could start to resemble the structure of the PCIP, which isn’t sustainable in the long run without huge premium increases.

The ACAs Looming Premium Hikes are Big – How We Can Lower Them

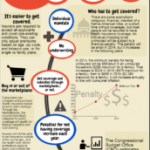

It’s been almost three years since the ACA was signed into law, and in that time, the implementation process has been both steady and plagued with difficulties. The major provisions of the law have largely adhered to the original scheduled time frames, but there have been numerous hiccups along the way, culminating last summer in a Supreme Court case that challenged the legality of several aspects of the law. Once SCOTUS ruled in favor of the ACA, the path was largely cleared for implementation of the health insurance exchanges (marketplaces) that are scheduled to be open for business this fall with policies effective next January. The individual mandate will also take effect in January, but the penalty for not having health insurance in 2014 will be very small ($95 per uninsured person, or 1% of taxable household income). This has caused some concern that the mandate might not be strong enough to avoid the looming problem of adverse selection: specifically, that people who are in need of healthcare might be much more likely to purchase health insurance than people who are currently healthy once all plans are guaranteed issue.

Last month I wrote an article about how the ACA will largely erase the differences that currently exist between the small group and the individual health insurance markets. Once that happens, it would be odd to expect to not see a corresponding change reflected in the premiums. I think it’s unlikely that the premiums will equalize via a drop in small group premiums (if anything, the requirement that small group plan deductibles not exceed $2000 might mean that the average small group premiums increase too). The individual market is poised to become more like the small group market once the policies become guaranteed issue, and the premiums in the small group market are currently significantly higher than the premiums in the individual market. There will likely be a price decrease for people at the upper end of the age spectrum in the individual market, since their premiums are going to be limited to a maximum of 3 times the premiums for young people. But there is a growing concern that those young people – and probably a lot of people in the middle too – might be in for some sticker shock.

Yes, the subsidies will help cushion the blow for people earning less than 400% of federal poverty level. But that still leaves a lot of people facing higher premiums and no subsidies. People who aren’t poor but definitely aren’t wealthy either – in other words, people who are middle class. Some of them are probably quite healthy. Some of them might have money stashed away in HSAs in order to pay for unexpected medical bills. Some of them might be happy to opt for higher deductibles and “catastrophic” health insurance plans in trade for lower premiums. But the way the ACA is currently written, they won’t be allowed to do that. The “catastrophic” plans will only be available to people under the age of 30 or people who meet the economic hardship qualifications. Everyone else will have to have at least a “bronze” plan that provides a broad range of benefits mandated by the ACA.

Yes, the subsidies will help cushion the blow for people earning less than 400% of federal poverty level. But that still leaves a lot of people facing higher premiums and no subsidies. People who aren’t poor but definitely aren’t wealthy either – in other words, people who are middle class. Some of them are probably quite healthy. Some of them might have money stashed away in HSAs in order to pay for unexpected medical bills. Some of them might be happy to opt for higher deductibles and “catastrophic” health insurance plans in trade for lower premiums. But the way the ACA is currently written, they won’t be allowed to do that. The “catastrophic” plans will only be available to people under the age of 30 or people who meet the economic hardship qualifications. Everyone else will have to have at least a “bronze” plan that provides a broad range of benefits mandated by the ACA.

Please don’t misunderstand me here. I firmly believe that our healthcare system needed […]

Patients Not Impressed By Recommendations For Less Preventive Care

Peggy Salvatore did an excellent job hosting the most recent Health Wonk Review – the Valentine’s Day Edition. I found this article by David Rothman, published at Health Affairs, to be particularly interesting. Although there has been much talk over the past few years about comparative effectiveness research, evidence-based medicine, and over-utilization of healthcare, patients… Read more about Patients Not Impressed By Recommendations For Less Preventive Care

The Downside Of Limited Benefit Association Health Plans

We recently worked with a client who is a Colorado REALTOR and a member of the National Association of REALTORS. She mentioned that she was eligible for coverage through NAR, but wanted to compare her options in the individual market with the policies that she could get as a NAR member. She sent over the details for us to look at, and we noticed that the coverage that NAR was touting as a benefit for members is basically just a guaranteed-issue limited benefit indemnity plan. Members have a choice of three different policy designs: The Physician Plan ($200/month for our client’s family of four) doesn’t include any inpatient benefits at all; it covers up to $100 per visit for office visits and ER visits, and up to $1000 for accidents. The Value Plan ($300/month for our client’s family) and Platinum Plan (almost $500/month) included limited inpatient and surgery benefits, but even the Platinum plan capped its benefits at $1000/day for inpatient care and $3000 per operating session for inpatient surgery. The plans are all guaranteed issue, but they have a 12 month pre-existing condition exclusion for any hospital or surgical expenses.

NAR makes it clear on their website – for people who are detail oriented – that the coverage offered through the REALTORS Core Health Insurance is not major medical and that the benefits are limited. They also provide a good informational page on their site about the struggles that self-employed people face when it comes to securing health insurance, and the efforts that NAR has made and continues to make in terms of making true group health insurance available to independent contractors who are part of a large association-type group like NAR. Presumably all of this will be a moot point as of next January when the individual mandate and guaranteed issue individual health insurance are implemented, but for now, it does appear that NAR is cognisant of the problems faced by many self-employed people who are trying to obtain medically-underwritten individual health insurance.

My concern is […]

Committee Kills Bill That Would Have Repealed Colorado Exchange Law

Colorado Representative Janak Joshi (R, Colorado Springs) is continuing his efforts to get government out of healthcare, but his latest bill died in a 9-2 vote in the House Health, Insurance and Environment Committee, with the no votes coming from both political parties. Joshi’s defeated bill would have repealed the 2011 law that created Colorado’s… Read more about Committee Kills Bill That Would Have Repealed Colorado Exchange Law

Value Based Health Insurance Plan Design Pilot Program Shows Promise

[…] With HSA-qualified plans, there have long been concerns that policy-holders are more likely to avoid necessary as well as unnecessary treatments, in an effort to save money. This is because the plan structure usually doesn’t cover any costs except preventive care until the insured has met the deductible. With the sort of value-based plan design being tested in the San Luis Valley HMO program, care that has a high level of evidence-based backing might be covered with no cost-sharing, while other treatments require some financial contribution from the patient. So it’s not the same as an HSA-qualified plan’s structure that just relies on a high deductible to deter a patient from seeking excessive care. And instead of putting all of the burden on the patient, the value-based insurance design incorporates a team approach, with involvement from patients, doctors and health insurance carriers. All in all, it seems like an excellent idea.

Colorado Lawmakers Push Ahead On Medicaid Expansion

Lawmakers in Colorado voted last week to reject a Republican proposal that education funding be a higher priority for the state budget than Medicaid expansion. In my opinion, the state’s Medicaid expansion plan is a good idea, and one that’s worth funding. The alternative is that we continue to have a significant segment of the… Read more about Colorado Lawmakers Push Ahead On Medicaid Expansion

Non-Mainstream Healthcare News

Maggie Mahar hosts this week’s Health Wonk Review, with a focus on waste in the healthcare system. It’s an excellent edition, full of great articles. Two of my favorites are stories that might not be covered in the mainstream news – but thanks to excellent healthcare bloggers, we still get to read them. Joe Paduda… Read more about Non-Mainstream Healthcare News